Post 1: Cracking the World Order

« On ne fait pas d’omelette sans casser des œufs. »

You can’t make an omelette without breaking eggs.

Since the 1700s, this French proverb has been used as a convenient justification for political sacrifice, serving as an all-purpose defense for harsh measures taken in pursuit of a greater goal.

That it’s French is no accident. Revolutionary France was a proving ground for the belief that violence in service of ideals isn’t just necessary: it’s righteous.

That same logic echoed through the 20th century, invoked by revolutionaries, hijacked by tyrants, and now, half a century after Bretton Woods, reappears in the polished kitchens of U.S. economic strategy.

Robespierre cracked eggs with zeal. Stalin scrambled them into purée. And now, half a century after Bretton Woods, U.S policy makers are back at the stove, pans clattering, shells flying.

Tariffs, immigration choke‑points, and ridiculous economic policies prompt commentators to wave the smoke away and declare the kitchen out of control, proof no one is really in charge. But what if the mess is deliberate? What if the splatter is the point?

This series of posts builds on this premise:

Chaos can be engineered.

Volatility can be weaponized.

In the 21st century, power is enforced less by armies and treaties but rather through pressure: economic, informational, and psychological.

The omelette metaphor is more than garnish. It is the organizing principle: break the right eggs at the right moment, and the shape of the meal — the world order — changes.

2. America’s Favourite Spatula: Intentional Instability

When U.S. influence curdles, Washington historically rarely tidies the kitchen. In fact, they usually turn up the heat.

Let’s look at how it has historically cooked with chaos.

1933 — FDR’s Bank Holiday.

Froze every bank account, took the dollar off the peg to gold, and threatened to pack the Supreme Court. It sparked short-term panic, but gave FDR the leverage to push through sweeping New Deal reforms.1971 — The Nixon Shock.

Nixon unilaterally ended the dollar’s convertibility to gold. Allies howled, markets spiraled, but floating exchange rates gave the U.S. monetary freedom and cemented dollar dominance that endures to this day.1980s — Reagan’s Military Buildup.

Europe feared Cold War escalation. But the U.S. spending blitz forced the USSR into an arms race it couldn’t afford: collapsing the Soviet economy without firing a shot.

Tariffs today reprise a familiar role. Headlines scream “fix the trade gap,” but their real function is subtler yet more potent. Tariffs inject uncertainty into pricing models, supply chains, and business expectations. That uncertainty creates political leverage.

And leverage becomes the legal rationale for invoking emergency powers that let the President bypass Congress. Each cracked egg becomes a pretext to grab another from the carton.

And this volatility isn’t just directed at Beijing. It hits U.S. firms, markets, and consumers deliberately. The resulting tension lays the groundwork for invoking wartime statutes and national-security provisions. In this light, tariffs aren’t just economic instruments; they are legal scaffolding for expanding executive authority.

This isn’t hypothetical. We’ve already seen how quickly disruption is repackaged into authority.

On his first day back in office, Trump declared a national emergency at the southern border, allowing him to deploy the military and redirect Pentagon funds to border enforcement and construction projects. That same day, he declared a national energy emergency, compelling agencies to accelerate domestic energy development. Within weeks, his administration issued executive orders imposing reciprocal tariffs and new trade restrictions, all framed as responses to economic threats.

This sequence wasn’t an accident.

It exemplifies a pattern in which crises, whether related to immigration, energy, or trade, are used to justify the expansion of presidential authority. By framing ordinary policy objectives as emergency responses, the executive can bypass legislative friction and push through sweeping measures with reduced oversight.

This strategy not only accelerates implementation but also sets dangerous precedents, steadily normalizing the use of emergency powers in domains that were once governed by debate and process.

Now, that same crisis playbook, engineered disruption to justify executive action, is bleeding into trade and economic policy.

Which brings us to the present: Why is the executive branch increasingly reaching for unilateral power? Why risk global blowback? Why play with fire in the supply chain?

The answer lies not in strength, but in vulnerability.

To understand that fragility, we have to zoom in, not on headlines, but on the balance sheet.

Hairline Fractures in the Shell — Why the Chef Is Nervous

Before tariffs were introduced, traditional macro dashboards flashed green: GDP is rising, unemployment hovers near record lows, and headline inflation has cooled.

But if you zoom in we will notice the countertop is riddled with cracks.

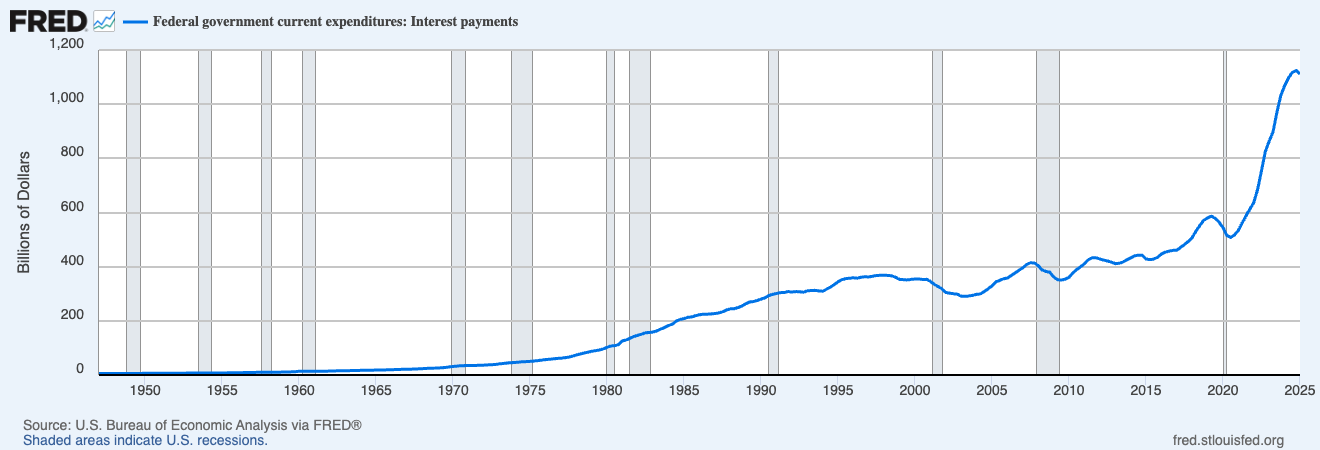

First: The $9 Trillion Refinancing Cliff.

1. The $9 Trillion Refinancing Cliff

Almost $9.2 trillion of Treasury debt matures this year, with another ≈ $17 trillion rolling off between 2025-2027. Rolling that pile at post-pandemic rates has already shoved annual interest expenses past $1.1 trillion—more than Washington spends on either Medicare or defense. Each basis-point tick higher in the federal funds rate bleeds billions more. (See image below)

2. Banks Hiding in Plain Sight

COVID stimulus stuffed banks with deposits. Lenders plowed that cash into “risk-free” long-dated Treasuries and agency MBS, then parked the bonds in held-to-maturity buckets to dodge mark-to-market pain. When the Fed lifted rates, those safe assets went radioactive:

Bank of America alone holds roughly $600 billion in HTM bonds with ≈ $132 billion in unrealized losses. Mark them today and its Tier-1 capital ratio plunges from 11.9 % to 3.8 %; Silicon Valley Bank territory. (Source)

These losses stay hidden only if deposits stay put and regulators keep the mask on. Another rate spike or a wave of deposit flight could turn this from a bookkeeping issue into a solvency crisis. Regulators aren’t blind to the problem, but they’re constrained in what they can do without risking broader panic. For now, they’re not fixing the system; they’re managing perception and hoping confidence in the system holds.

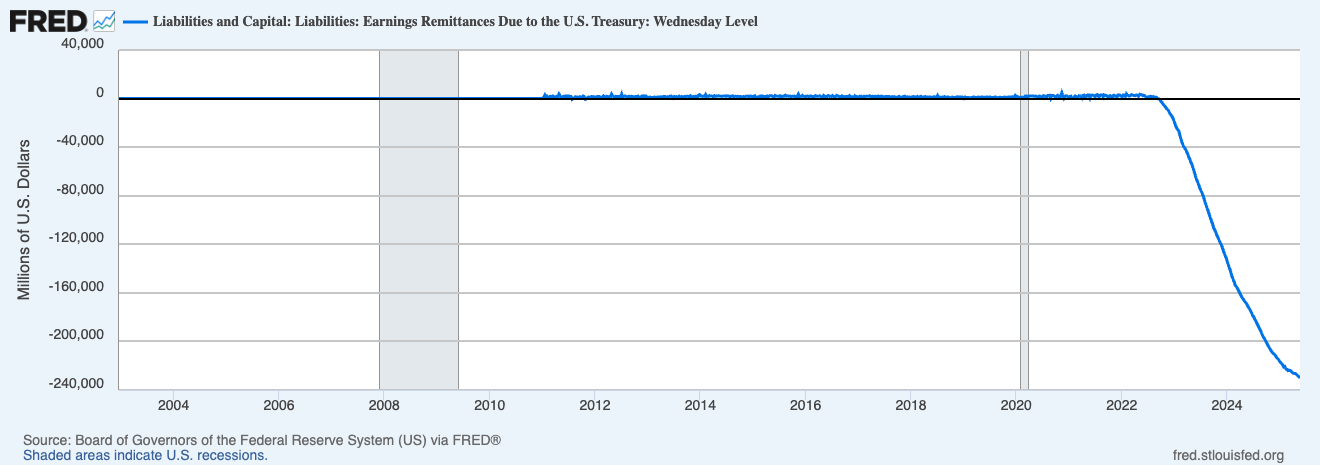

3. A Federal Reserve Bleeding Cash

The Fed is in uncharted territory. It earns just ~1.8% on its $7 trillion pile of long-term bonds, while paying ~5.4% interest on bank reserves and ~5.3% on reverse repos. That’s called negative carry, when the cost of funding exceeds the return on assets.

The result? The Fed is losing money every day, and it’s stopped sending its usual $100+ billion in annual remittances to the Treasury—remittances that used to quietly ease budget strain. (See image below).

Bottom line: America isn’t collapsing. But its foundation is weakening. Empires in that state don’t back off—they scramble faster and harder, betting that heat and motion can hold it together before everything curdles.

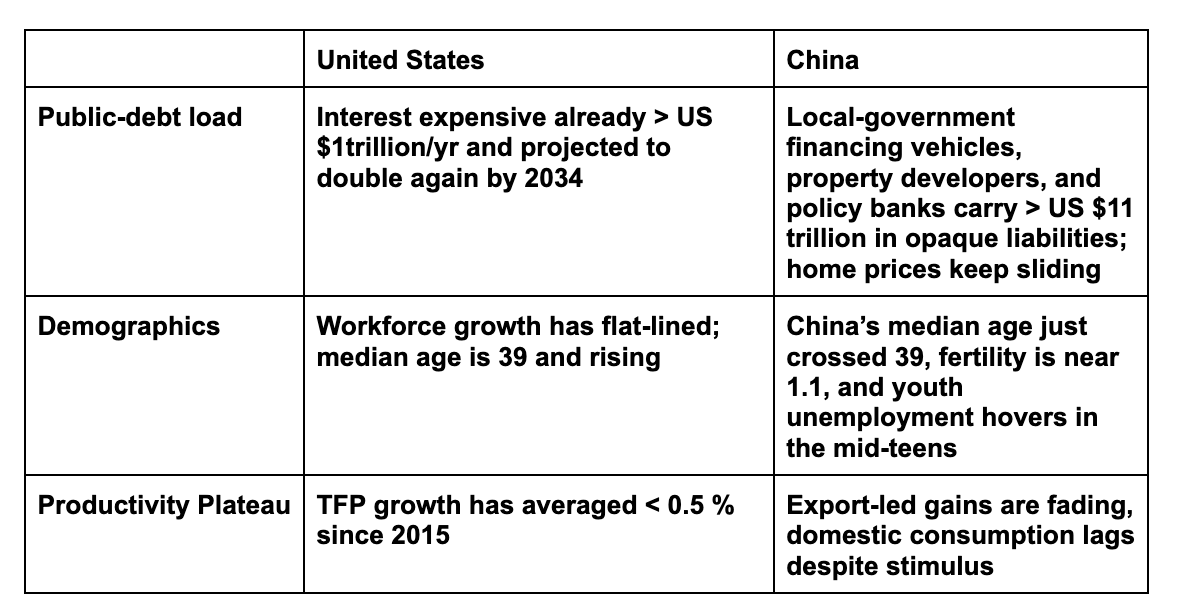

4. Two Cooks, One Skillet—The U.S. and China Scramble for AI

Beneath the ideological theatre, Washington and Beijing balance on the same wobbly three‑legged stool: high debt, ageing demographics, and low growth.

Interest rates are trapped for opposite reasons. Washington keeps them high to tame inflation; Beijing keeps them low to kindle growth, yet demand still lags. Workforces on both shores are shrinking, and neither government dares whisper the scarlet word austerity. Talks of spending cuts, tax hikes, or pension reform are political suicide.

In America, the political center has collapsed. Stimulus triggers inflation panic. Immigration fuels culture wars. And any talk of cutting Social Security or Medicare dies on arrival.

In China, the ruling party can’t afford to show weakness. Youth unemployment has reached historic highs. Local governments are overwhelmed by hidden debt. And each round of credit stimulus risks either inflating another bubble or triggering foreign pushback.

That leaves just one lever big enough to shift the equation without detonating careers: artificial intelligence.

What once felt like a niche technology now borders on macroeconomic necessity. It offers what neither politics nor monetary policy can: a way to grow out of stagnation without touching pensions, borders, or ideology.-

It replaces labor without importing it, boosts GDP without raising deficits, and, after a burst of capital spending, offers scale without sacrifice.

Seen through that lens, AI could act as a tool for balance-sheet triage.

Whichever power captures the first AI dividend gets to dictate technical standards, monopolize chip and compute supply, and walk into negotiations from a position of calm, not panic.

But the skillet is small. GPUs, high-NA EUV scanners, rare-earth magnets; these are all finite.

The only real question is: who gets served first, and who’s left scraping the pan while the others sweep up eggshells? That’s where tariffs come in. They’re no longer just taxes on goods. They’re strategic wedges. Export controls on Dutch lithography, tighter rules on U.S. cloud access, quotas on critical minerals: all designed to starve rivals of the hardware and raw inputs needed to scale.

Washington isn’t acting from confidence. It’s trying to tip Beijing’s stool just enough to slow things down and buy time before its own foundation cracks. The goal isn’t collapse—it’s delay: long enough to figure out how to stay on top. It’s a gamble, and one that’s getting harder to hide.

5 · Where We Go Next

Post 2 will crack open tariffs themselves—what they can scramble and what they can’t. We’ll track how Washington wields softer tools, dollar dominance and supply-chain choke-points, to achieve what taxes on imports alone never could.

The omelette isn’t finished. But the eggs are continuing to break.